As California begins the slow crawl back to economic stability, Florida remains stuck in the swampland of the economic downturn. The similar circumstances of the two states at the height of the Great Recession leave many questioning what differences led to a swifter recovery pace in the West. The more efficient foreclosure process in the Golden State is the key.

California completes the vast majority of its foreclosures through a nonjudicial foreclosure process, also known as trustee’s sales, and thus does not require foreclosures to be approved by a judge, as is the case in Florida. While court involvement may be helpful to those homeowners who didn’t fully understand the risk involved in the mortgage they acquired, the process is much more tedious and time consuming.

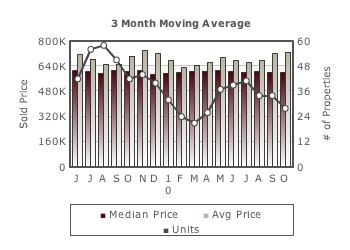

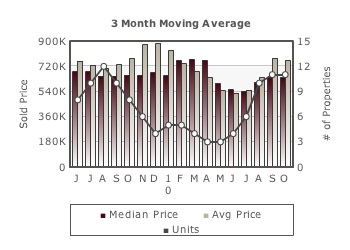

A faster method of clearing out foreclosures along with a more dynamic economy has provided California with the means to an upturn before Florida. Home prices in Los Angeles are up 10% from their bottom, San Diego is up 14% and San Francisco up 21%. Miami prices are up a measly 2% from their all-time low, and Tampa prices are still falling.

first tuesday take: Florida is to California what California is to the recovery which could be taking place, if lenders would either process their backlog of foreclosures, or acquiesce to forgiving principal indebtedness, i.e., cramming down loan balances for underwater homeowners. Just as judicial foreclosures extend Florida’s economic recovery in comparison to California’s economic recovery, lender foot-dragging extends California’s recovery.

For economic recovery to speed up, lenders need to quit refusing cramdowns and delaying foreclosures in hopes of retaining their solvency. California may be more efficient than other states, but that isn’t saying much. The process is certainly not without its blemishes, the biggest being lenders’ lack of participation in the effort to save our California economy and keep homeowners in their homes, something they will have no small interest in going forward when they will want to be everyone’s financial partner.

An efficient system for addressing delinquency is necessary, but not at the expense of fairness. Rather than halting foreclosure altogether, we must re-examine the laws governing lender oversight and fight for stricter legal recourse when lenders refuse to foreclose or borrowers experience unfair foreclosures in the future. After all, it is the owner who defaults and by doing so exercises his put option to require the lender to take the property, and nothing else.

For More InformationPlease contact me if you'd like more information about our community or real estate market:

Walter Stauss, Lifestyles Real Estate500 Seabright Avenue, Santa Cruz, California 95062Cell: 831.246.4663, Email: walter@831.com, Web: http://www.831.com DRE #01105052